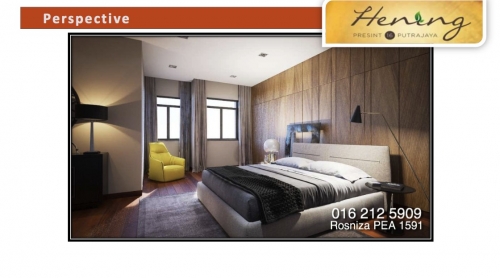

Ejen Hartanah Bandar Baru Bangi, Bandar Bukit Mahkota, Cheras, Kajang, Putrajaya, Seri Kembangan, Nilai, Semenyih, Puchong, Kuala Lumpur, Sepang, Salak Tinggi, Putra Height

Sebelum anda membeli rumah pastikan anda periksa dahulu kelayakan pinjamanan yang boleh anda mohon. Selain daripada minta nasihat pihak bank anda juga boleh membuat pengiraan sendiri supaya anda dapat merancang nilai rumah yang boleh anda beli dan memudahkan pinjaman anda lulus. Ini adalah langkah-langkah pengiraan pinjaman bank untuk anda:

1- Kira Pendapatan Bersih

2- Kira Had Maksima DSR (Debt Service Ratio)

3- Net Disposable Income (NDI)

4- Kira Kelayakan Komitmen Baru

5- Kira Harga Rumah Maksima

#1 KIRA PENDAPATAN BERSIH

PENDAPATAN (INCOME)

– Dividen ASB

– Dividen TH

– Sewaan*

– Komisen*

*Mungkin tidak diambil pada nilai 100%

[-] PENOLAKAN (DEDUCTION)

[=] PENDAPATAN BERSIH (NET INCOME)

#2 KIRA HAD MAKSIMA DSR (DEBT SERVICE RATIO)

PENDAPATAN – PENOLAKAN = PENDAPATAN BERSIH

[x] KADAR PERATUS DSR

– Bank

– Pendapatan Bersih

HAD MAKSIMA DSR

– Komitmen sedia ada

– Komitmen baru

#3 NET DISPOSABLE INCOME (NDI)

Gaji Bersih RM 3,000

#4 KIRA KELAYAKAN KOMITMEN BARU

HAD MAKSIMA DSR

[-] KOMITMEN SEDIA ADA

[=] KELAYAKAN KOMITMEN BARU

#5 KIRA HARGA RUMAH MAKSIMA

KELAYAKAN KOMITMEN BARU

[x] PEMALAR

– Kadar efektif 4.5%

– Tempoh Pembiayaan 35 tahun

[=] HARGA RUMAH MAKSIMA YANG LAYAK DIBIAYAI

– Harga rumah RM 100,000

#CONTOH 1 (CUKUP NDI)

PENDAPATAN: GAJI (RM 3,000) + ELAUN TETAP (RM 1,000) = RM 4,000

[-] PENOLAKAN: KWSP (RM 240) + SOCSO (RM 20) + ZAKAT (RM 50) = [-] RM 310

#1 PENDAPATAN BERSIH = RM 3,690

#2 HAD MAKSIMA DSR

Andaian bank tersebut menggunakan kadar peratus DSR 60%

#3 NDI

Komitmen Sedia Ada: Tiada

#4 KELAYAKAN KOMITMEN BARU

#5 HARGA RUMAH MAKSIMA YANG LAYAK DIBIAYAI

#CONTOH 2 (TAK CUKUP NDI)

PENDAPATAN: GAJI (RM 2,000) + ELAUN TETAP (RM 500) = RM 2,500

[-] PENOLAKAN: KWSP (RM 160) + SOCSO (RM 12) + ZAKAT (RM 10) = [-] RM 182

#1 PENDAPATAN BERSIH = RM 2,318

#2 HAD MAKSIMA DSR

Andaian bank tersebut menggunakan kadar peratus DSR 60%

#3 NDI

KOMITMEN SEDIA ADA: Tiada

#4 KELAYAKAN KOMITMEN BARU

#5 HARGA RUMAH MAKSIMA YANG LAYAK DIBIAYAI